by

User Not Found

| Nov 13, 2023

The enactment of SECURE Act 2.0 has introduced significant changes aimed at strengthening the retirement system and enhancing Americans’ financial preparedness for their golden years. While this legislation encompasses a range of provisions, one

area that directly affects families’ planning for education is the ability to make penalty- and tax-free rollovers from 529 plans to Roth IRAs, starting in 2024.

How SECURE Act 2.0 enhances 529 rollovers

In addition to the broader improvements in retirement planning, SECURE Act 2.0 has paved the way for more flexible educational savings. By allowing penalty- and tax-free rollovers from 529 plans to Roth IRAs, families can now optimize their savings while

ensuring their loved ones’ educational needs are met.

Key points regarding 529 rollovers to Roth IRAs

- Ownership of Roth IRA: The Roth IRA must be in the name of the 529 beneficiary, not the owner.

- 529 plan duration: The 529 plan must have been open for a minimum of 15 years to be eligible for rollovers.

- Recent contributions exclusion: Rollover amounts cannot include 529 contributions made in the preceding five years.

- Maximum rollover: The lifetime maximum amount that can be rolled over from a 529 account into a Roth IRA is $35,000 per beneficiary.

- Rollover limitations: Rollovers are subject to the annual Roth IRA contribution limit and are reduced by any contributions made by the beneficiary into their Roth or traditional IRA. ($7,000 in 2024)

- Earned income: To be eligible to rollover 529 assets to a Roth IRA, the 529 beneficiary must have earned income equal to or greater than the annual limit being rolled over to the Roth IRA.

Benefits and considerations

There are additional things to think about when considering a 529 rollover to a Roth IRA. First, this strategy can increase accessibility for high-income earners. Unlike traditional Roth IRA contributions, this opportunity bypasses income phase-out rules,

making it accessible for high-income families.

It also offers flexibility in planning. Families now have the flexibility to strategically plan their educational savings, ensuring financial security while addressing educational needs.

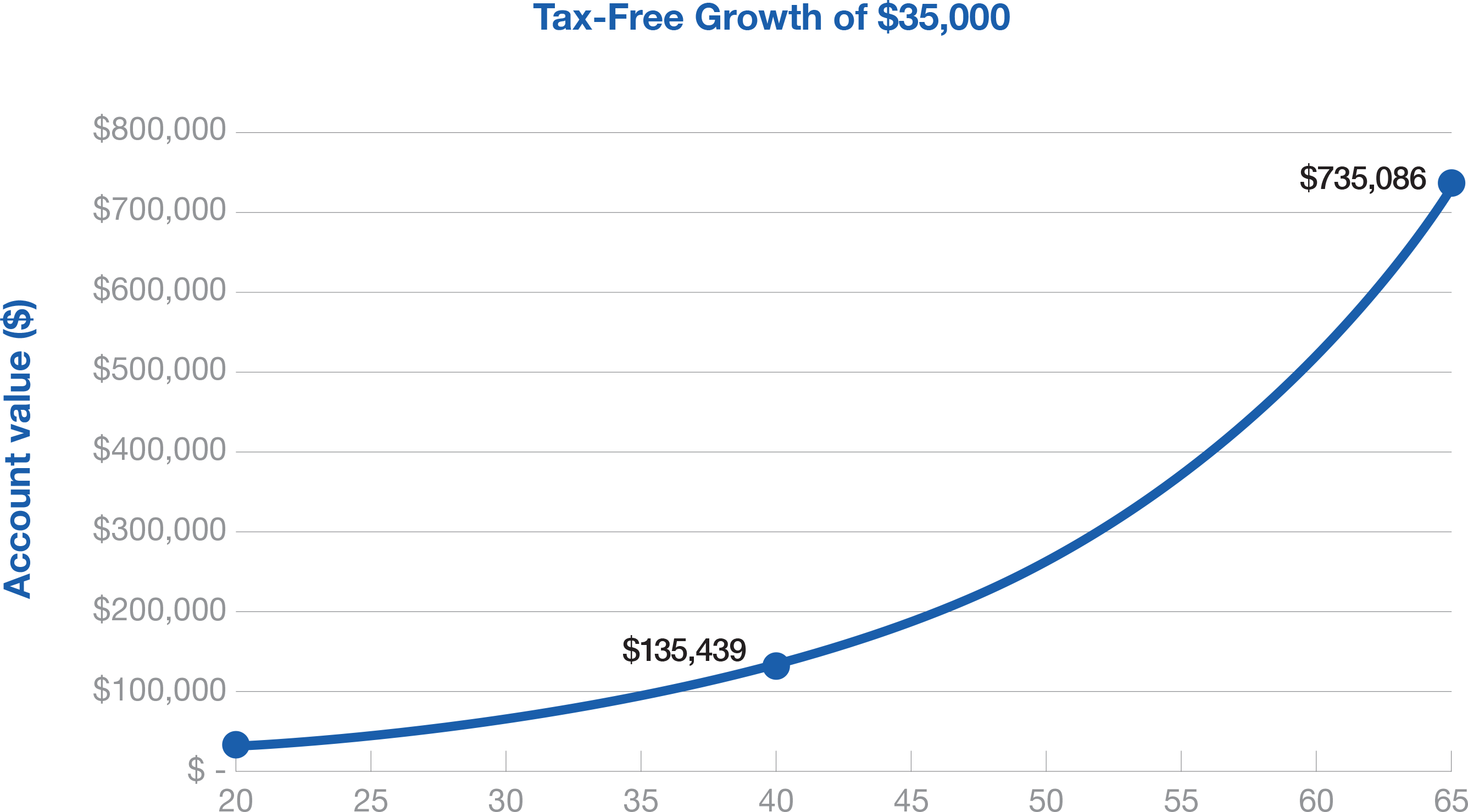

By understanding the nuances of 529 rollovers to Roth IRAs, families can make informed decisions, optimizing their savings and ensuring a brighter educational journey for their loved ones. To help put the power of tax-free investment earnings into perspective,

the graph below illustrates growth on $35,000 over a 45-year time horizon.

While this may look compelling, every individual’s financial landscape is unique. Variables such as income, savings goals, and personal circumstances play a significant role in making the most of these changes. That's why it’s imperative to

consult with a financial advisor or tax professional. Our team can help you navigate the intricacies of SECURE Act 2.0, ensuring that you make informed decisions tailored to your specific needs and aspirations. Contact us anytime.